October 2022

Buy Now, Pay Later Tracker® Series

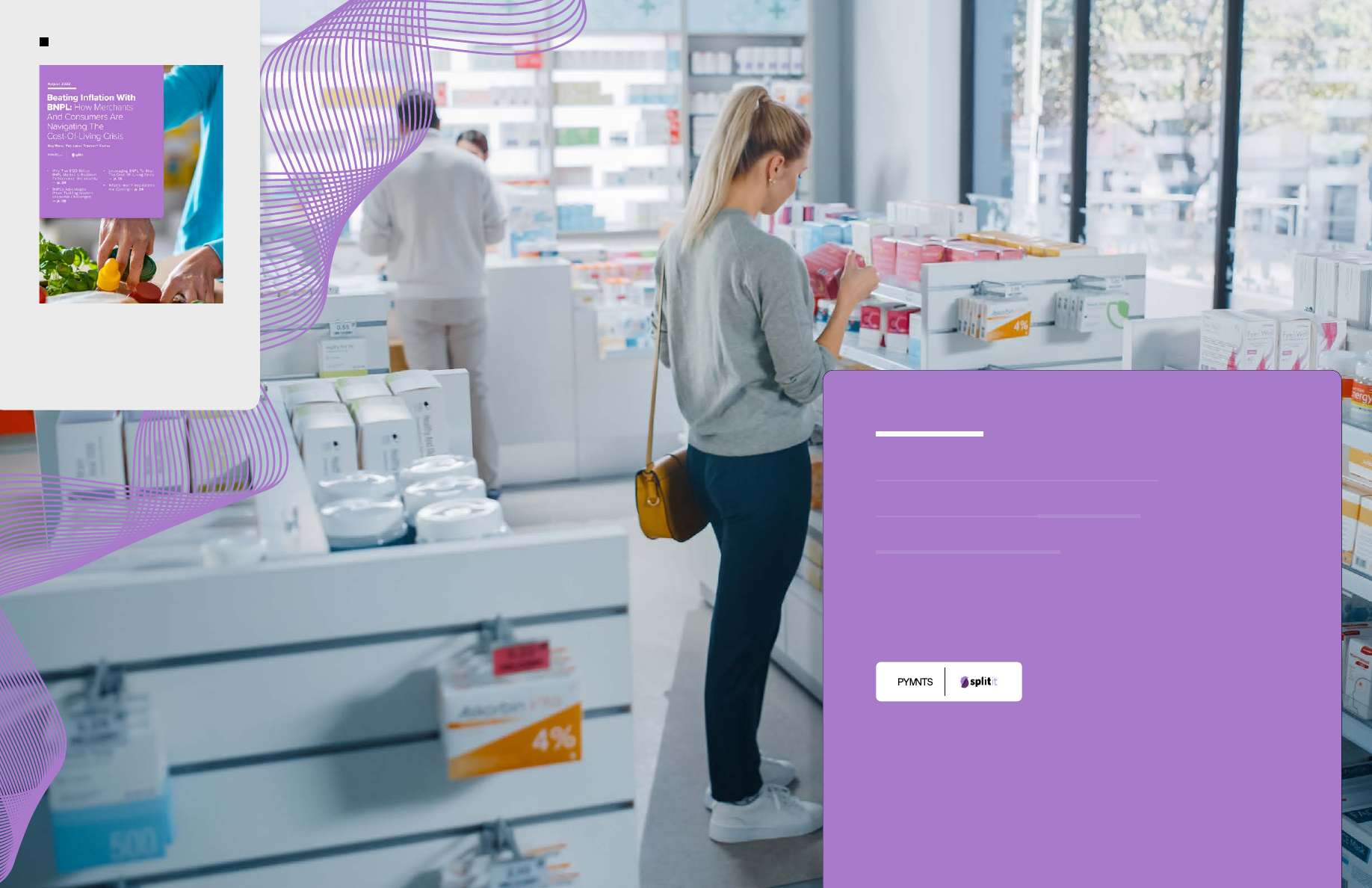

Unlocking The True

Potential Of BNPL

For Services

• BNPL Expands Access To

Services — p. 04

• Medicine, Education

Are The New BNPL

Applications — p. 10

• Breaking Down BNPL

Habits — p. 14

• Merchant Halts Discounts

After BNPL Offering

— p. 16